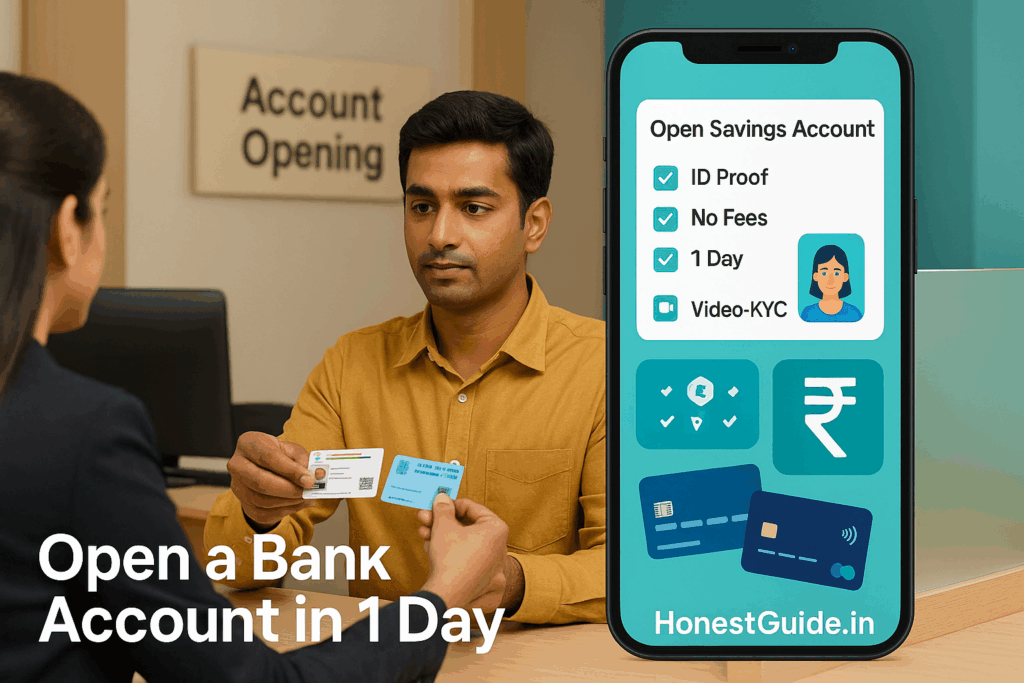

Open a Bank Account in 1 Day (Docs, Fees & Steps)

Open a Bank Account in 1 Day (Docs & Fees)

Want a working savings account today—for salary credit, UPI, IMPS/NEFT, and debit card? This guide gives you the fastest routes (branch + digital), the minimum documents, what fees to expect, and what to say if anyone slows you down. We also include scripts and the exact escalation ladder (all official).

Quick note: RBI allows multiple onboarding modes—face-to-face, video-KYC (V-CIP), and non-face-to-face Aadhaar OTP e-KYC. Pick what’s quickest for you. Reserve Bank of India

🧭 Summary

-

Outcome: Get a usable savings account same day via branch (full KYC) or online with Video-KYC/e-KYC, then start UPI immediately once credentials arrive. State Bank of India+2HDFC Bank+2

-

Timelines: Digital onboarding often completes within minutes to a few hours; branch accounts are usually same working day if documents are in order. (Banks advertise instant activation; actual time varies by bank.) HDFC Bank+1

-

Costs: BSBD/zero-balance accounts must offer core services free (no minimum balance). Other accounts may have monthly average balance (MAB), debit card annual charges, and cheque-book fees—check the bank’s tariff. Reserve Bank of India+1

-

Docs: Any Officially Valid Document (OVD) (Passport/Driving Licence/Voter ID/PAN/Aadhaar letter/NREGA job card), plus PAN (or Form 60 if no PAN). Aadhaar OTP e-KYC and DigiLocker e-documents are acceptable in digital journeys. Reserve Bank of India+2Reserve Bank of India+2

-

Top pitfall: Confusing BSBD (zero-balance) with BSBD-Small (limits: ₹1,00,000 credits/year; ₹50,000 max balance) used when full KYC isn’t done. Know the difference before you choose. Reserve Bank of India

🧰 Before you start

Who this is for: First-timers, students, busy professionals, seniors—anyone needing a savings account quickly, including NRIs visiting India (NRIs will need NRE/NRO variants; process differs).

What you’ll need (pick one route):

-

Branch (full KYC): One OVD for identity + address, PAN (or Form 60), 2–4 passport photos (some banks take live photo). Reserve Bank of India

-

Video-KYC / Digital: Aadhaar (for OTP or offline XML) + PAN, good data connection, well-lit video call, and your live location enabled. Many banks also accept DigiLocker documents. Reserve Bank of India

-

Already have CKYC? Share your KYC Identifier and consent so the bank can download your records from CKYCR—less paperwork. Reserve Bank of India

Costs & TAT:

-

BSBD (Basic Savings Bank Deposit) account: No minimum balance; core services free. Reserve Bank of India+1

-

Regular savings variants: Expect debit-card annual fee, SMS alerts, cheque-book charges, and MAB penalties if applicable—bank tariff rules apply (varies by bank; check the schedule of charges).

Where to do it:

-

Digital (fastest): Bank app or website—look for “Insta/Quick/811/Video-KYC/Online Savings”. HDFC Bank+2State Bank of India+2

-

Branch: Walk in with originals; ask for same-day activation after full KYC.

🔟 Steps (do this now)

1) Choose account type: BSBD (zero-balance) or regular.

If you want no minimum balance and free basic services, choose BSBD. If you need premium features (higher free withdrawals, premium card), choose a regular plan and maintain MAB. Reserve Bank of India+1

2) Decide onboarding mode.

-

Fastest at home: Video-KYC or Aadhaar OTP e-KYC (subject to bank’s process).

-

Reliable at branch: Face-to-face KYC (good if your address proof isn’t Aadhaar or you prefer human help). Reserve Bank of India

3) Keep documents handy.

-

OVD list: Passport, Driving Licence, Voter ID, PAN, Aadhaar letter, NREGA job card (Govt-notified OVDs). Reserve Bank of India+1

-

No PAN? Use Form 60 (some digital journeys also accept it). (Check the bank’s specific flow.)

4) If you have a CKYC number, use it.

Tell the bank your KYC Identifier and give explicit consent for them to download your records from CKYCR—saves time and duplication. Reserve Bank of India

5) Start the application (app/site or branch).

Select “Open savings account,” choose plan, fill details. For digital: enable camera, mic, and location; keep Aadhaar-linked mobile ready.

6) Complete KYC:

-

Video-KYC (V-CIP): Join the bank’s secure video call; show OVDs on camera; respond to random prompts; confirm current location. Reserve Bank of India

-

Aadhaar OTP e-KYC (non-face-to-face): Enter Aadhaar; consent to OTP authentication; note that accounts opened via OTP e-KYC have specific conditions under RBI’s KYC Directions (banks may require full CDD within a specified timeline). Reserve Bank of India

-

Branch KYC: Show originals; sign forms; provide photo and specimen signature.

7) Choose delivery & credentials.

Set up mobile banking, internet banking, UPI, and pick card delivery. Many banks enable UPI as soon as the customer ID is activated (some features may wait till card/PIN arrives).

8) Fund (if required) and verify activation.

BSBD needs no initial deposit; regular accounts may require first funding. Check SMS/email for account details and try a ₹1 UPI receive to confirm activation (where enabled). Reserve Bank of India

9) If offered a “Small”/limited account, know the caps.

BSBD-Small (used when full KYC is pending) has ₹1,00,000 total yearly credits and ₹50,000 max balance at any time. Convert to full KYC soon to remove caps. Reserve Bank of India

10) Save your evidence bundle.

Screenshots of the application, KYC consent, ticket numbers, tariff sheet, and welcome email/SMS. Useful if anything breaks later.

📋 Checklist (copy-paste)

-

Decide BSBD vs Regular (no MAB vs extra features).

-

Pick onboarding mode (Video-KYC / Aadhaar OTP e-KYC / Branch).

-

Keep OVD + PAN (or Form 60) handy.

-

If available, share CKYC Identifier and give consent for download.

-

Complete KYC (video/OTP/branch).

-

Enable UPI, mobile & net banking.

-

Note charges (debit card, SMS, cheque book, MAB).

-

If opened as Small/limited, schedule full KYC conversion.

-

Save application proof (screenshots, emails, SMS).

-

Do a test transaction (₹1 receive/send).

⚠️ Red flags & common mistakes

| Mistake | Consequence | Fix |

|---|---|---|

| Picking a Small/limited account unintentionally | Caps on balance (₹50,000) and total yearly credits (₹1,00,000) | Ask specifically for full KYC or convert soon after opening. Reserve Bank of India |

| Bank insists on minimum balance for BSBD | You pay avoidable fees | Remind staff that BSBD must offer basic services free with no minimum balance. Reserve Bank of India+1 |

| Refusing Form 60 when you don’t have PAN | Application stalls | Politely ask for Form 60 option (RBI-permitted); provide PAN later if required. (Check bank’s process.) |

| Video-KYC fails due to poor lighting/network | Delay or rejection | Sit near a window, stable internet, keep OVDs ready; reschedule session. Reserve Bank of India |

| Not giving CKYC consent when you have a CKYC ID | Re-uploading all docs | Share your CKYC number and consent so the bank downloads your KYC record. Reserve Bank of India |

🗣️ Templates & scripts

A. Branch script (BSBD request)

“Namaste. I want to open a Basic Savings Bank Deposit (BSBD) account today. I have [OVD] and PAN/Form 60. As per RBI, BSBD has no minimum balance and offers basic services free. Please process it now and confirm same-day activation.”

B. Video-KYC support chat

“Hello. I’m trying to complete V-KYC for my savings account. My Aadhaar and PAN are ready; please share the next available video slot and any location/lighting requirements.”

C. CKYC consent line

“I already have a CKYC/KYC Identifier. I consent to your bank downloading my KYC records from CKYCR for onboarding.”

D. Email to branch manager if delayed beyond 1 working day

Subject: Request for same-day activation – savings a/c (Application #[ID])

Dear [Manager Name],

I applied to open a savings account on [date/time] with full KYC completed ([mode: branch/video/OTP]). Request expedited activation today. Attaching application receipt/screenshots.

Thanks,

[Name], [Mobile], [CKYC/KYC ID if any]

🧗 Escalation path (with links)

-

Bank customer care / branch manager – ask for ticket number and TAT.

-

Bank’s Nodal/Grievance Officer – find on the bank’s website (“Grievance Redressal”).

-

RBI Integrated Ombudsman (RB-IOS) – file online on the RBI Complaint Management System (CMS) (24×7). Keep your bank ticket and documents handy. Reserve Bank of India+1

❓ FAQs

1) Which documents are accepted as OVD?

Passport, Driving Licence, Voter ID, PAN, Aadhaar letter, and NREGA job card (Govt-notified). Banks may also accept DigiLocker e-documents and Aadhaar (OTP/biometric) for digital KYC journeys per RBI’s KYC Directions. Reserve Bank of India+2Reserve Bank of India+2

2) Can I open an account without visiting a branch?

Yes. RBI permits Video-KYC and non-face-to-face Aadhaar OTP e-KYC; many banks offer instant digital accounts. Some features/cards may follow later. Reserve Bank of India+2State Bank of India+2

3) What is BSBD vs BSBD-Small?

BSBD = zero-balance with core services free. BSBD-Small is a temporary/lite account until full KYC is done; caps: ₹1,00,000 total credits/year and ₹50,000 max balance. Reserve Bank of India+1

4) I don’t have PAN yet. Can I still open an account?

Yes—use Form 60 where the bank allows, then update PAN. (Check your bank’s policy.)

5) I already completed CKYC elsewhere. Can the bank reuse it?

Yes—give your KYC Identifier and explicit consent; the bank can download your records from CKYCR. Reserve Bank of India

6) Will Aadhaar OTP e-KYC accounts have limits?

RBI’s KYC Directions set conditions for accounts opened via OTP e-KYC in non-face-to-face mode; banks may require full CDD within a timeline. Ask your bank how they handle this. Reserve Bank of India

7) How fast can I start using UPI?

Often same day once the customer ID/account is live and mobile is linked; timelines vary by bank. HDFC Bank+1

8) Do BSBD accounts really have no minimum balance?

Yes. RBI requires no minimum balance and basic services free for BSBD accounts; banks can’t downgrade BSBD because you didn’t buy extras. Reserve Bank of India+1

9) Whom do I complain to if a branch delays or misinforms me?

Escalate to the bank’s nodal officer; if unresolved, file on RBI CMS under the Integrated Ombudsman Scheme. Reserve Bank of India+1

10) Are there bank examples of instant digital accounts?

Yes—major banks advertise digital accounts with Video-KYC/Aadhaar-based onboarding (names and features vary). Check each bank’s current offer. HDFC Bank+2State Bank of India+2

📚 Sources

-

RBI – FAQs on Master Direction on KYC (June 9, 2025) — onboarding modes (face-to-face, V-CIP, non-face-to-face e-KYC), acceptance of e-documents/DigiLocker, CKYC consent. Reserve Bank of India

-

RBI – Master Direction on KYC (and V-CIP definition/standards) — legal basis for Video-KYC and non-face-to-face accounts; conditions for Aadhaar OTP e-KYC. Reserve Bank of India+1

-

RBI – BSBD/BSBDA Circular & FAQs — zero-balance policy and free basic services. Reserve Bank of India+1

-

RBI – BSBDA-Small limits — ₹1,00,000 yearly credits, ₹50,000 max balance. Reserve Bank of India

-

RBI – Integrated Ombudsman Scheme FAQs & CMS complaint portal — how to file complaints online (24×7). Reserve Bank of India+1

-

CKYC/CKYCR (CERSAI) – FAQs & operating info — customer consent and KYC Identifier usage. CKYC India+1

Disclaimer: This is general information, not financial advice. Fees/features can change—always check your bank’s latest tariff and terms before applying.