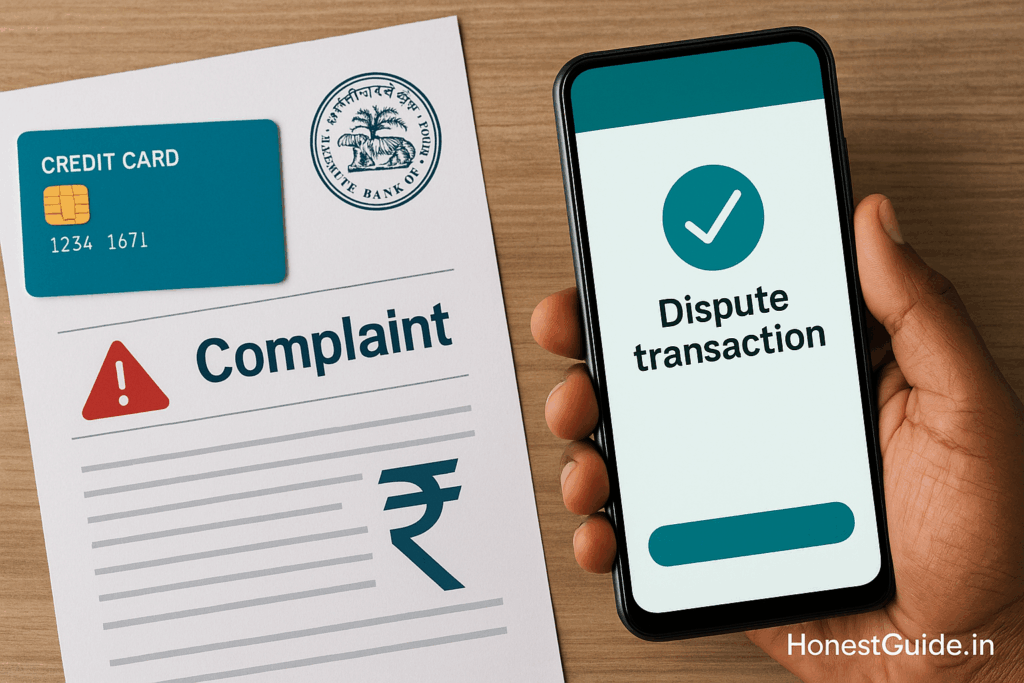

Dispute a Credit Card Charge in India (Fast, Step-by-Step)

Dispute a Credit Card Charge in India

A wrong or fraudulent card charge is fixable—if you act fast and document well. This guide tells you exactly what to do today, what forms to file, what to say to your bank, and when to escalate to the RBI Ombudsman if the bank stalls.

🧭 Summary

-

Outcome: Get an incorrect/unauthorised credit card transaction reversed (chargeback/refund) or receive a temporary credit during investigation. Typical resolution: 45–90 days (network/issuer dependent). SBI Card

-

Timelines that matter: Report fraud ASAP; report within 3 working days = zero customer liability under RBI rules. If the bank doesn’t resolve or respond in 30 days, escalate to RBI Ombudsman (CMS portal). Reserve Bank of India+1

-

Costs: No fee to dispute. Interest/late fees should be held if a temporary credit is given; keep paying undisputed dues to avoid penalties (ask for fee reversal if wrongly applied). (Derived from issuer policies.)

-

Docs: Card statement screenshot, merchant invoice/chat/email, delivery proof, police e-FIR for clear fraud, screenshots of app/OTP logs, and the bank’s Transaction Dispute Form (TDF). SBI Card

-

Top pitfall: Waiting too long—many issuers require disputes within 30–90 days (e.g., ICICI 90 days; SBI Card 90 days for Visa/Mastercard/Amex, 30 days for RuPay domestic). ICICI Bank+1

🧰 Before you start

Who this is for: Anyone in India who sees a card transaction that’s fraud/unauthorised, billed twice, not received goods, charged wrong amount, or merchant refused refund.

What you’ll need:

-

Latest statement highlighting the disputed txn(s).

-

Merchant communication (emails/chats/tickets).

-

Proof of non-delivery/return (tracking, denial notes).

-

Screenshots (bank app alerts, SMS, OTP you did/didn’t share).

-

TDF (Transaction Dispute Form) from your issuer (download or raise online/app). SBI Card+1

Where to do it: Bank app/portal (raise dispute), customer care, email to grievance, and, if needed, RBI Ombudsman (CMS portal). RBI CMS+1

Turnaround times (typical):

-

Temporary credit during investigation: case-by-case.

-

Final resolution (chargeback cycle): ~45–90 days depending on network/merchant response. SBI Card

Key protections:

-

Report unauthorised transactions within 3 working days → zero liability; limited caps if reported within 7 days; beyond that, bank policy applies. Reserve Bank of India

🔟 Steps (do this now)

-

Freeze exposure

Block the card in your bank app or call helpline; request a replacement card. (Prevents further misuse.) -

Raise the dispute with your bank (same day)

Use your bank’s dispute feature or TDF. Examples: HDFC online dispute form, SBI Card TDF, ICICI dispute ticket (banks vary; follow on-screen steps). HDFC Bank+2SBI Card+2

Tip: Select the right reason (fraud, duplicate, not received, credit not processed). -

Ask for a temporary credit

If appropriate, request a provisional/temporary credit so you’re not penalised while the bank investigates. (SBI Card notes this practice.) Keep paying undisputed dues. SBI Card -

Assemble your evidence bundle

Attach statement, merchant emails/invoices, delivery/return proof, screenshots of bank alerts/SMS. For clear fraud, add e-FIR number (where applicable). -

Get the service request (SR) number in writing

Note the date/time, SR/ticket number, and the channel used (app/call/email). -

Respond quickly to bank queries

Banks may ask for clarifications or documents (e.g., signed letter, ID). Submit within the stated window to keep the case alive. (Issuers highlight time-bound documentation.) SBI Card -

Track timelines

Mark T+30 days from your complaint. If unresolved or you get an unsatisfactory reply, you can approach the RBI Ombudsman (CMS). Reserve Bank of India -

Escalate inside the bank first (optional but helpful)

Email the grievance/nodal officer of your bank quoting the SR and attaching evidence, asking for a written position within 7 working days. (Banks publish nodal contact routes.) HDFC Bank -

File with RBI Ombudsman (if needed)

Use RBI Complaint Management System (RB-IOS 2021); upload your evidence and bank correspondences. You may also send a physical complaint to RBI’s Centralised Receipt and Processing Centre, Chandigarh, per RBI FAQ. Reserve Bank of India+1 -

Close the loop

When resolved, check your statement for reversal/credit and any interest/late fee; ask the bank in writing to reverse residual charges arising from the disputed txn.

Notes

-

Window to raise disputes varies by issuer/network. Example policies: ICICI up to 90 days, SBI Card: 90 days (Visa/Mastercard/Amex), 30 days (RuPay domestic). Check your bank’s page for the exact window. ICICI Bank+1

-

Full chargeback cycles can run 45–90 days or as per card network rules. SBI Card

📋 Checklist (copy-paste)

-

Card blocked & replacement requested

-

Dispute raised (app/web/TDF) + SR number saved

-

Evidence bundle prepared & uploaded

-

Temporary credit requested (if applicable)

-

Calendar marked for T+30 days follow-up

-

Bank grievance/nodal officer escalated (if needed)

-

RBI Ombudsman complaint filed on CMS (if unresolved/unsatisfactory after 30 days)

-

Final credit verified; fees/interest reversed

⚠️ Red flags & common mistakes

| Mistake | Consequence | Fix |

|---|---|---|

| Waiting beyond issuer window (e.g., 30–90 days) | Bank may refuse to raise chargeback | Raise dispute immediately; cite issuer page; keep SR proof. ICICI Bank+1 |

| Not reporting fraud within 3 working days | You may bear part/all liability | Report ASAP; RBI gives zero liability if reported within 3 working days. Reserve Bank of India |

| Deleting SMS/emails | Lose evidence | Keep all alerts; take screenshots; save PDFs. |

| Not paying undisputed dues | Interest/late fees pile up | Pay minimum on undisputed amount; seek reversal of fees linked to the disputed txn. |

| Escalating to RBI too early | Case may be returned | Wait until 30 days after complaint to bank or after receiving unsatisfactory reply. Reserve Bank of India |

🗣️ Templates & scripts

A) Email to Bank (Initial Dispute)

Subject: Dispute of Credit Card Transaction(s) — [Last 4 digits XXXX] — SR request

Body:

Hello,

I am disputing the following transaction(s) on my credit card [last 4 digits XXXX]:

-

Date/Time: [DD-MM-YYYY, HH:MM]

-

Merchant: [Name]

-

Amount: ₹[ ]

-

Reason: [Unauthorised/Not received goods/Duplicate/Wrong amount/etc.]

Evidence attached: statement highlight, merchant communication, delivery/return proof, screenshots.

Please register my complaint, share the SR number, and confirm temporary credit pending investigation.

Regards,

[Name, Mobile, Email, Address]

B) Phone script (for customer care)

“Namaste. I need to dispute a credit card transaction. Card ending XXXX. Transaction on [date], merchant [name], amount ₹[ ]. Reason: [fraud/duplicate/not received]. Please block my card, issue replacement, lodge the dispute, and share the SR number by SMS/email. I will email supporting documents today. Please confirm if temporary credit applies.”

C) Escalation to Nodal/Grievance Officer

Subject: Request to expedite unresolved card dispute — SR [#####]

Body:

Hello,

My dispute SR [#####] dated [DD-MM-YYYY] remains unresolved. I’m attaching the evidence bundle and prior correspondence. As per bank policy and RBI RB-IOS, kindly provide a written resolution within 7 working days, failing which I will approach RBI Ombudsman (CMS).

Regards,

[Name]

D) RBI Ombudsman (CMS) complaint summary

Issue: Disputed credit card transaction(s); bank failed to resolve within 30 days / provided unsatisfactory reply on [date]. Relief sought: Charge reversal and reversal of related charges/interest.

🧗 Escalation path (with links)

-

Your Bank (Issuer) — App/web dispute, customer care, email. (Use issuer’s TDF/online form; e.g., HDFC online dispute, SBI Card TDF.) HDFC Bank+1

-

Bank Grievance/Nodal Officer — Email the bank’s published grievance route with SR and evidence (e.g., HDFC nodal contact page). HDFC Bank

-

RBI Ombudsman (RB-IOS 2021) — RBI Complaint Management System (CMS) online; physical complaints accepted at RBI CRPC, Chandigarh as per RBI FAQ. Reserve Bank of India+1

❓ FAQs

1) How long does a chargeback take?

Usually 45–90 days, depending on card network rules and merchant response times. SBI Card

2) What if the transaction is clearly fraudulent?

Report immediately; under RBI rules, if you report within 3 working days, your liability is zero. The bank must investigate and reverse unauthorised debits. Reserve Bank of India

3) Is there a deadline to raise my dispute?

Yes—issuer/network specific. Examples: ICICI up to 90 days; SBI Card 90 days (Visa/Mastercard/Amex), 30 days (RuPay domestic). Check your bank’s page. ICICI Bank+1

4) Do I need to keep paying my bill?

Pay undisputed amounts. Ask for a temporary credit and reversal of any fees/interest tied to the disputed txn. (SBI Card notes temporary credits during investigation.) SBI Card

5) The bank hasn’t responded in 30 days. What now?

Escalate to the RBI Ombudsman via CMS with your SR, evidence, and bank correspondence. Reserve Bank of India+1

6) Is UPI different from card disputes?

Yes, UPI is governed by NPCI with its own dispute TATs and processes; this guide is for card charges. (NPCI circulars frequently update UPI TATs.) NPCI+1

7) Will I always get a temporary credit?

It’s case-by-case; ask explicitly. Banks may post provisional credits while they investigate. SBI Card

8) Can the bank refuse my dispute?

Yes, if evidence is weak or filed late. Strengthen your case with clear documents and timely filing; if you disagree, use the grievance route and then RBI Ombudsman. Reserve Bank of India

📚 Sources (official/primary)

-

RBI — Customer Protection: Limiting Liability in Unauthorised Electronic Banking Transactions (06 Jul 2017) — zero/limited liability timelines (3/7 days). Reserve Bank of India

-

RBI — RB-IOS 2021: Complaint & escalation via Complaint Management System (CMS) + 30-day guidance in FAQs. Reserve Bank of India+1

-

RBI — FAQs on Master Direction for Credit & Debit Cards (Mar 2024) — CMS and postal complaint details (CRPC Chandigarh). Reserve Bank of India

-

SBI Card — Customer Grievance/Customer Liability Policy — chargeback resolution 45–90 days; timelines and practices. SBI Card

-

Issuer windows/examples:

-

ICICI Bank — Dispute status page (notes 90-day window). ICICI Bank

-

SBI Card — Transaction Dispute FAQs & TDF (PDF) (windows; temporary credit). SBI Card+2SBI Card+2

-

HDFC Bank — Online Cardholder Dispute Form (how to submit). HDFC Bank

-

Disclaimer: This is general consumer-rights guidance, not legal or financial advice. Fees/policies change—check your issuer’s page and RBI site for current rules.